SUMMARY

Retained directly by Intuit's QuickBooks Partner leadership in early 2021 to design the next-stage QBO partner channel from a blank sheet. Six months and four connected workstreams: a new partner taxonomy, a behavior-led incentive framework, a wholesale partner certification pathway, and a refreshed Resale and Referral Agreement. The program shipped at the inflection point where Online crossed from a slim majority of segment revenue to roughly two-thirds, and was sized for the channel QBO was becoming, not the one it had been.

| Organization | Intuit Inc., Small Business & Self-Employed Group (now Global Business Solutions) |

| Function | QBO Partner Channel Architecture (sole external designer): Taxonomy, Behavior-Led Incentives, Wholesale Certification, Resale & Referral Agreement |

| Engagement Sponsor | A former Microsoft colleague, then a Vice President at Intuit, leading the QuickBooks Partner organization |

| Duration | January 2021 to mid-2021, six months of design work refined across more than a dozen iterations with Intuit leadership |

The Origin: A Call from a Former Colleague

In January 2021 I got a call from a former colleague, then a Vice President at Intuit, who had taken on the global QuickBooks Partner organization. He had watched my channel partner architecture and program efforts at Microsoft, and he was looking at a structurally similar problem on his own franchise. Intuit had a partner program that had been built for a license-led desktop business now sitting on top of a subscription-and-attach platform business that was about to overtake it.

His brief was direct: redesign the QuickBooks Online partner channel from a blank sheet of paper, not by optimizing or bolting onto the existing Desktop program. The sequence would run taxonomy first, then incentive economics, then a certification gate, then the commercial agreement that bound the whole thing together. The channel QBO was becoming, not the channel it had been.

THE BRIEF

The Brushton Group was retained directly by Intuit's QuickBooks Partner leadership to design the next-stage QBO partner ecosystem from the ground up, in time for the inflection point where Online would cross from a slim majority of the SB&SE segment to roughly two-thirds of it.

The Inflection Point

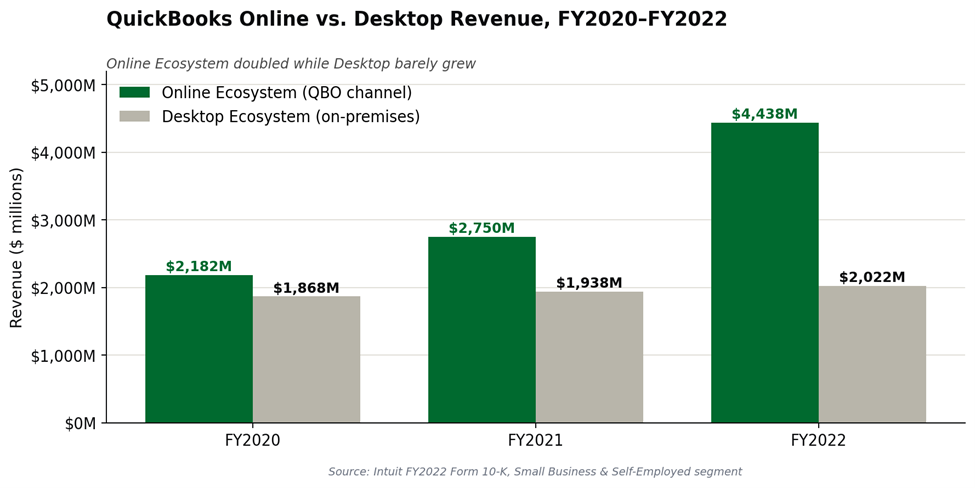

Intuit operates one of the largest small-business software channels in the world. By early 2021 the QuickBooks franchise sat at a structural turning point. The Online Ecosystem (the QBO subscription channel and its attach economy of payroll, payments, Capital, and marketing) generated about $2.18B of segment revenue. Desktop generated about $1.87B. Online held a slim majority, but the partner program had not been redesigned for that mix.

Two years later the picture was unrecognizable. Online more than doubled to $4.44B while Desktop barely grew. The program had to be sized for where the channel was going, not where it had been.

The result, by the end of 2020, was a partner experience with overlapping incentives, inconsistent terms across partner types, and a certification pathway that did not match the cloud-era partner profile QBO needed at scale. Behaviors that drove durable QBO retention and expansion (renewal management, services attach, multi-year commitments) were either uncompensated or compensated alongside logo-capture behaviors that did not produce a durable customer.

KEY INSIGHT

Most SaaS partner programs were built for the transaction era and have not been redesigned for the renewal-and-expansion era. The QBO redesign was a deliberate move to the latter: behavior-led economics, certification as a financial gate, and commercial agreements written to follow the operating model rather than lead it.

The Design: Six Months, Four Connected Workstreams

I ran the engagement across four connected workstreams over six months, refined across more than a dozen iterations with Intuit leadership and the partner field. None of the four existed in the prior program in the form that shipped. It was a greenfield design, sequenced deliberately. Taxonomy first, because nothing else can be designed cleanly until the field has agreed who counts as what kind of partner. Then the incentive framework that the taxonomy implied. Then certification as the financial gate. Then the commercial paper that turned the operating model into contracts.

1. Partner Taxonomy

A clean classification of the partner types that touch QBO and a precise definition of each type's rights of participation. The redesign separated activities that had collapsed into single partner labels in the prior program: who sells, who services, who bills, who manages renewals, who owns expansion, and who is rewarded for what. Each partner type was given distinct economics tied to its actual contribution to the QBO business rather than a tier badge derived from prior-year volume.

The taxonomy distinguished six investment vehicles, each mapped to specific products, behaviors, and partner motions. The same vocabulary was used in every downstream document so that contracting, compensation, and field operations could speak in one language.

| Vehicle | Construct | Mechanic | Where it applies |

|---|---|---|---|

| Wholesale Billing | Discount from MSRP | Partner resells; Intuit bills the partner; partner sets price to customer | QBO, QBO AV, Online Payroll, QB Time, QBES, Hosting, FSM, POS |

| Residual | Ongoing % | Ongoing payment for sales activity; fixed dollar or % of sale | QBES, Payroll, Hosting, FSM, POS (time-bound going forward) |

| Fee (Bounty) | One-time | One-time payment at successful sale where partner does not resell | QBO, QBO AV, Online Payroll, QB Time, QBES, Plus, Hosting |

| Rebate | Performance-based | Quarterly payment to partner based on attainment to sales goals | Cross-portfolio, paid alongside other incentives |

| MDF | % reinvested | Marketing development funds reinvested against agreed partner plan | QBO, QBO AV, Payroll, QB Time, QBES, Plus, Hosting, FSM |

| Custom | Strategic, >10 only | Bespoke quarterly performance contract for the largest strategic partners | Strategic products and markets |

2. Behavior-Led Incentive Framework

A principles-led design for how QBO compensates partners, anchored on an explicit decision between rebate-led and fee-led mechanics for each motion. The framework was deliberately built around behaviors that drive QBO retention and expansion rather than behaviors that capture a logo without producing a durable customer. The taxonomy from workstream one fed directly into the incentive framework, where each partner type was tied to the behaviors its compensation model was designed to reward.

Tier rates were re-cut against the new taxonomy. Elite, Executive, Strategic, Advanced, and Member tiers received differentiated economics across QuickBooks Enterprise, Subscription, Hosting, Payroll, Payments, and the QBO Bounty stack.

| Compensation line | Elite | Executive | Strategic | Advanced | Member |

|---|---|---|---|---|---|

| QBES GNS Commission Bonus | 30% | 30% | 30% | 25% | 25% |

| QBES Subscription Residual (incl. Upgrade) | 20% | 15% | 10% | 10% | 5% |

| QBES Hosted Commission | 28% | ||||

| FSM Licenses Residual | 25% | 20% | |||

| Intuit Payments Profit Share (referral) | 40% | 35% | |||

| Online Payroll Bounty (Elite tier) | $500 | ||||

| QBO Bounty (Simple Start / Essentials / Plus / Adv) | $50/$100/$150/$300 | ||||

| Marketing Development Funds per quarter | $5,000 | $3,000 | $2,000 | $1,000 |

OPERATOR NOTE ON RATE-SETTING

The framework was designed to support "mass customization" in the rate sheet so that Intuit could change rates period-over-period, swap product targets as strategy moved, and pivot goal structures (GNS, growth, revenue) without re-papering the channel. The wholesale discount itself was held constant; incentives were the lever for responding to the market.

3. Wholesale Partner Certification

A new certification pathway built around the Wholesale Partner Certification Questionnaire. Certification was structured as evidence of capability rather than attestation of intent, and it was tied to a defined enablement curriculum that partner organizations had to complete before accessing wholesale economics. Certification became a meaningful gate. What sat behind it was financially significant enough that partners actually invested in the program rather than treating it as a checkbox.

4. Commercial Framework

The legal and operational terms that bound the ecosystem together. Outputs included a refreshed Resale and Referral Agreement issued in mid-2021, a clearer contracting flow between sell-through and refer-out paths, and updated business-process documentation that field operations could actually run against. The agreement architecture was deliberately written to follow the operating model rather than lead it. Document the operating model first, then write the paper the operating model implies.

Across all four workstreams, the design held the same principle. The incentive math is the easy part. The hard part is migrating partners from the program they have to the program they need, on a calendar that does not stall the existing motion. The migration plan, not the framework, separated this redesign from the half-finished ones it replaced.

What Shipped

Four shipped artifacts closed the redesign cycle and operationalized the new program.

- The Wholesale Partner Certification Questionnaire moved from concept to executable program, gating partner access to the redesigned wholesale economics.

- The Resale and Referral Agreement was issued in mid-2021, replacing the prior architecture and aligning contractual terms to the new partner taxonomy and incentive design.

- The incentive framework was deployed with documented partner economics structured to scale across the QBO partner base, with explicit decisions captured between rebate-led and fee-led mechanics.

- The taxonomy and business-process changes were operationalized for the field, with refreshed documentation that the operations team could actually execute against.

The Results

Within two fiscal years the QBO channel went from a slim majority of segment revenue to roughly two-thirds. That is unusually fast for a multi-billion-dollar software franchise. It is the shape of a successful managed migration, the same pattern Microsoft ran in its Enterprise Agreement-to-cloud transition on the productivity side.

- Online Ecosystem revenue more than doubled, from $2.18B in FY2020 to $4.44B by FY2022. Online surpassed Desktop as the larger franchise during the engagement window, and the gap widened in every subsequent quarter.

- The recurring revenue share of the segment crossed 80% in FY2022, the inflection point at which Intuit could credibly tell the public market it was a subscription company. The partner motion was sized for that compounding curve.

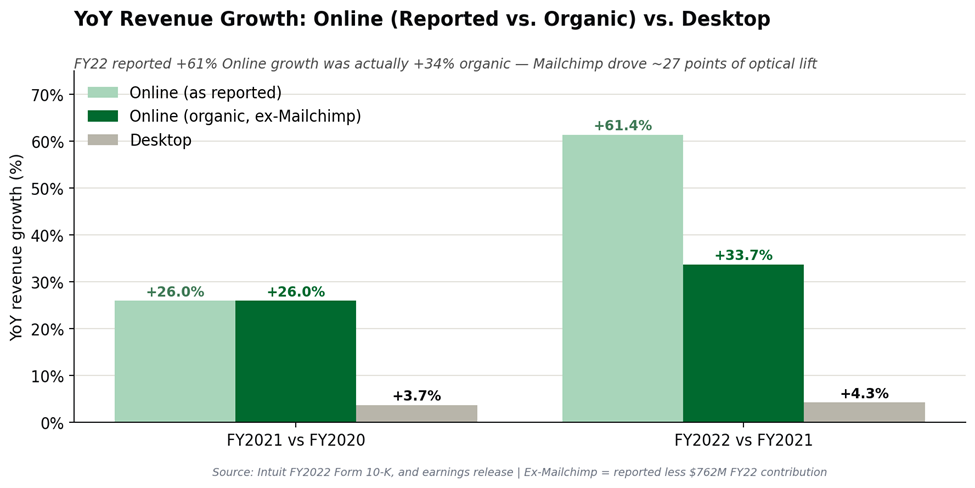

- QuickBooks Online Accounting compounded at 25% then 33% across FY2021 and FY2022 on subscriber growth and ARPC expansion through higher-tier mix and pricing actions. The pure SaaS subscription line, unaffected by any acquisition, was the cleanest validation that the partner economics were lined up correctly.

- By fiscal year 2025, Online Ecosystem reached approximately 75% of segment revenue, Online Services ($4.18B) had surpassed QBO Accounting ($4.12B), and the segment had been renamed Global Business Solutions. The attach economy the redesign was built around (payments, Bill Pay, Capital, payroll) became the dominant growth engine.

THE STRUCTURAL VALIDATION

Successful managed migrations look like this: the new business doubles, the old business holds steady, and the channel that runs both stays in sync with the customer. The redesigned QBO partner program was the lever that made the customer migration politically and economically tractable.

Six Operator-Level Patterns

Six patterns came out of this work that I now apply broadly to cloud-era partner ecosystems. These are the durable lessons.

- Incentive design has to follow partner behavior, not partner logos. Tier-only programs reward presence; behavior-led programs reward the activities that drive customer retention. The QBO framework rewarded renewal management, services attach, and multi-year commitments because those behaviors compounded the customer.

- Certification is most useful as a gate to economics, not a marketing badge. The QBO wholesale certification framework worked because what sat behind it was financially meaningful. Partners invested in it because it unlocked real money, and that investment was the actual point.

- A clean taxonomy is worth more than a clever framework. Partner types that overlap in rights or responsibilities create field confusion that no incentive design can resolve. Clarity at the taxonomy layer made every downstream decision easier.

- Migration design is the work. Moving partners from old terms to new terms is harder than the design itself. The framework on paper is the easy part. The migration plan is what separates a redesign that ships from one that stalls.

- Field operability beats elegance. A clever framework that the field operations team cannot run produces more chaos than a simpler one that operates cleanly. The test of any partner redesign is whether the team that runs it can actually run it on Monday morning.

- Commercial agreements should follow the operating model, not lead it. Document the operating model first. Then write the agreement that the operating model implies. Most teams do this backwards and end up with paper that does not match practice.

How The Brushton Group Applies This

The Brushton Group's commercial strategy practice brings operator-level experience to channel architecture, partner incentive design, and partner ecosystem strategy. Engagements work backward from a precise definition of the commercial outcome, then design the program, the incentive economics, and the operating mechanics that move partner behavior at scale. The QBO engagement is one of several channel redesigns the practice has led across cloud-era SaaS organizations facing the shift from license to subscription, with attach economics layered on top.

For organizations evaluating a partner program redesign, the right starting point is rarely the incentive math. It is definitional: what partner types actually exist, what each is rewarded for, and what the rights and responsibilities of each look like in the field. Get that right and the rest of the program design follows naturally. Get it wrong and no incentive structure will resolve the field confusion that overlapping rights create.

If this pattern is familiar, the Brushton Diagnostic is a useful starting point for evaluating where your commercial model stands. Or contact us directly to discuss your specific situation.

Appendix: The Numbers Behind the Channel Mix Shift

This appendix captures the public-record financial detail behind the channel redesign. It is intended for analysts, investors, and program designers who want the underlying mechanics. All figures are recognized revenue per Intuit's FY2022 and FY2025 Form 10-K filings.

A1. Segment Revenue Movement, FY2020 to FY2022

| Metric (Small Business & Self-Employed) | FY2020 to FY2022 movement |

|---|---|

| Online Ecosystem revenue | $2,182M to $4,438M (+103% reported, +68% organic ex-Mailchimp) |

| Desktop Ecosystem revenue | $1,868M to $2,022M (+8.2% over two years) |

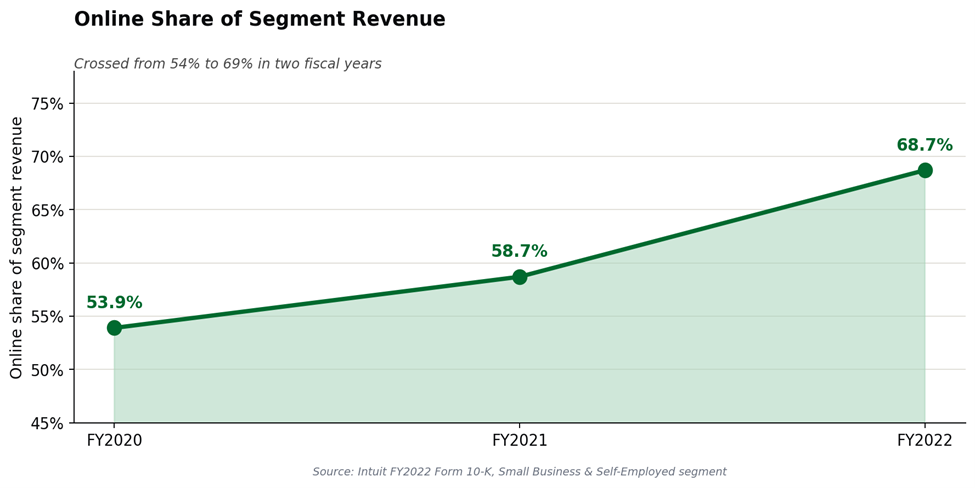

| Online share of segment revenue | 53.9% to 68.7% reported / 53.9% to 64.5% organic |

| Recurring share of segment revenue | 74.5% to 82.8% (subscriptions + services + recurring transactions) |

| QBO Accounting (core SaaS subscription) | $1,354M to $2,267M (+25% FY21, +33% FY22) |

| Online Services (attach economy) | $828M to $2,171M (payroll, payments, Capital, Mailchimp) |

| Desktop Accounting | $755M to $851M (largely price-led, not unit-led) |

| Desktop Services and Supplies | $1,113M to $1,171M (essentially flat in real terms) |

Source: Intuit FY2022 Form 10-K, Small Business and Self-Employed segment revenue tables; FY2022 Q4 earnings release (Mailchimp $762M FY2022 contribution).

A2. Online Growth: Reported vs. Organic

The Mailchimp acquisition closed November 1, 2021, and added roughly $762M of inorganic Online Services revenue in FY2022. Stripping that out reveals the underlying organic motion the partner program had to be sized for.

THE OPERATOR READ

By FY2022, Online Services ($2.17B) was effectively equal in size to QBO Accounting ($2.27B). The attach economy of payments, payroll, Capital, and marketing automation had become as large as the seat-license business. The partner conversation was no longer about distributing accounting software. It was about distributing financial services with bookkeeping as the wedge.

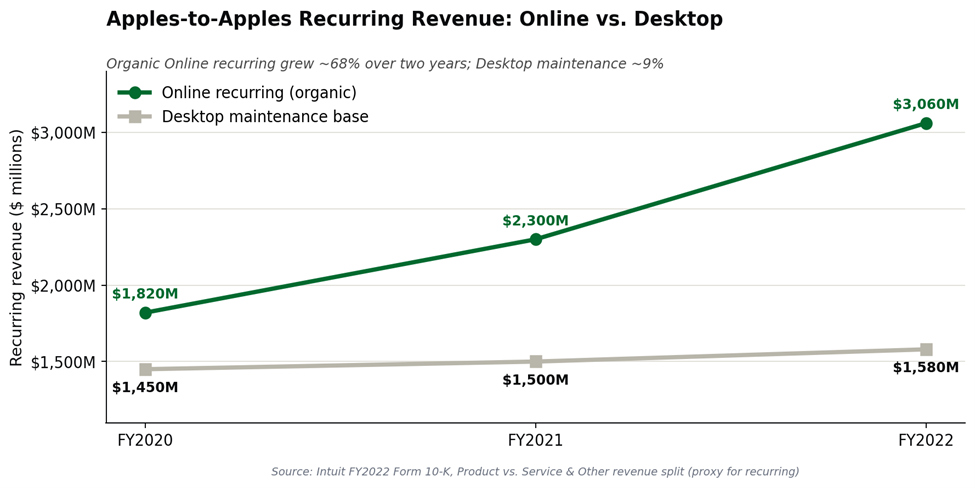

A3. Recurring Revenue: Online vs. Desktop Maintenance Base

The Desktop installed base pays maintenance every year and the QBO base is 100% subscription. Cutting the segment by recurring versus new (using Intuit's own Product versus Service and Other revenue split as a proxy) shows where the money actually came from. Organic Online recurring grew approximately 68% over two years against the Desktop maintenance base of approximately 9%. The Desktop maintenance annuity (services, supplies, subscription support) added $73M of revenue across the two years, an effectively flat result in real terms. Desktop new license shipments added another $81M. Combined, all of Desktop contributed about $154M, or roughly 6%, of the $2,410M of segment growth across the engagement window. The other 94% came from the Online side.

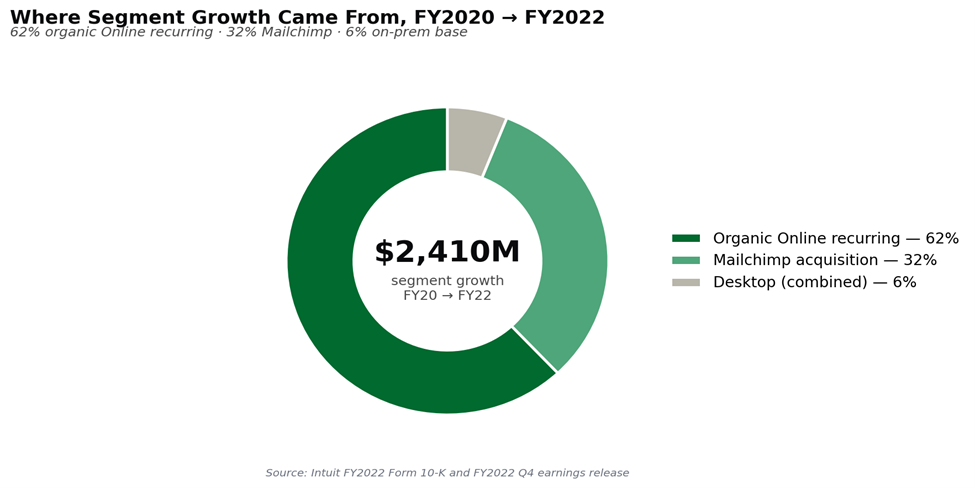

A4. Where Segment Growth Came From

The decomposition: 62% organic Online recurring, 32% Mailchimp acquisition, 6% combined new and recurring from the on-prem base. For a channel program designer, this is the decisive insight. The on-prem maintenance base is not a growth engine. It is a price-extracted annuity in managed decline. A partner whose economics depended on Desktop new license was tied to a contracting line. A partner who pivoted to QBO subscription plus payments and payroll attach was aligned to $1.5B of organic recurring growth. The partner program had to make that pivot economically rational at the partner-firm level.

A5. Online Share of Segment Revenue

Online share of segment revenue grew from 53.9% to 68.7% in two fiscal years.

A6. Sources & Methodology

Reported revenue figures are pulled directly from Intuit's FY2022 and FY2025 Form 10-K filings and the FY2022 Q4 earnings release. Two derived series in this appendix are constructed from those filings rather than reported as line items. The Online recurring (organic) and Desktop maintenance series are proxies built from Intuit's Product vs. Service and Other revenue split, allocated to Online and Desktop in proportion to each segment's reported revenue mix; this is a directional construction, not a reconciled line item. The Online (organic, ex-Mailchimp) growth strips out the $762M FY2022 Mailchimp contribution disclosed in Intuit's FY22 Q4 earnings release; the residual is treated as the underlying Online motion the partner program had to be sized for. Analysts reconciling against the 10-K should expect the reported totals to tie exactly and the derived series to differ within rounding.

Sources:

- Intuit Inc., Form 10-K, fiscal year ended July 31, 2022 (Small Business and Self-Employed segment revenue tables, Product vs. Service and Other revenue split, MD&A discussion).

- Intuit Inc., Form 10-K, fiscal year ended July 31, 2025 (Global Business Solutions segment, Mailchimp ex-revenue growth disclosures, Desktop subscription transition narrative).

- Intuit Inc., FY2022 Q4 earnings release and conference call (Mailchimp $762M FY2022 revenue contribution, approximately 80% subscription mix disclosure).

- Brushton Group engagement record: Resale and Referral Agreement (issued mid-2021); Wholesale Partner Certification Questionnaire (partner-facing); Partner Incentives Taxonomy and Review (April 2021); Incentives Framework offsite materials (2021).

About the Author

Brendan T. O'Connor is Founder and Principal of The Brushton Group, a strategy consulting practice delivering enterprise-grade commercial strategy for growth and scale. During his eighteen-year Microsoft tenure (1998 to 2016), he created the Enterprise Agreement direct-billing architecture, including the conversion from indirect sales to a direct, fee-based structure, the Partner compensation models, the fee schedules, and the geographic rollout. He subsequently led the Microsoft Dynamics Licensing Solutions team ("Deal Desk"). He then served as Senior Director of Worldwide Enterprise Partner Incentives where he managed and allocated a $1.2B budget. After Microsoft, he held senior commercial strategy roles at Cisco and Sage. He holds an MS in Industrial Administration (MBA equivalent) from Carnegie Mellon University's Tepper School of Business and a BS in Mechanical Engineering, also from Carnegie Mellon.

Contact: LinkedIn / Full Profile / [email protected]